Choosing between leasing vs buying is one of the most significant financial decisions you’ll face, whether you are looking at a new vehicle, specialized equipment, or even a home. There is no “one-size-fits-all” answer; the right choice depends entirely on your financial priorities, how long you plan to use the asset, and your desire for ownership.

In this guide, we’ll break down the pros and cons of each to help you decide which path aligns with your lifestyle.

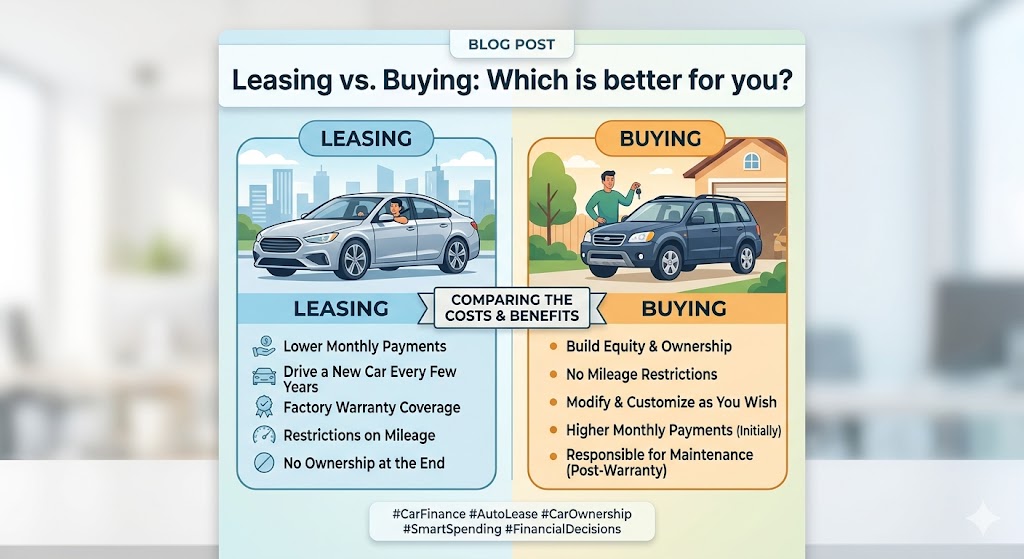

Understanding the Basics

- Buying: When you buy, you are paying for the total value of the asset. Once the loan is paid off, you own it entirely. It becomes part of your net worth, and you can sell it or trade it in whenever you like.

- Leasing: Leasing is essentially a long-term rental. You are paying for the depreciation of the asset during the time you use it. At the end of the lease term (typically 2 to 4 years), you return it to the owner or dealer.

The Pros and Cons at a Glance

| Feature | Buying | Leasing |

| Monthly Payments | Generally higher (paying for total value). | Generally lower (paying for depreciation). |

| Ownership | You own the asset once paid off. | You do not own the asset. |

| Customization | You can modify it however you like. | Must remain in original condition. |

| Maintenance | Your responsibility after warranty. | Often covered by the manufacturer. |

| End of Term | You keep it or sell for cash. | You return it or buy it at a set price. |

Key Factors to Consider

1. Your Monthly Budget

Leasing is often the most attractive option for those who want a “more expensive” asset for a lower monthly cost. Because you aren’t paying for the full value, your cash flow remains more flexible. Buying requires a larger upfront commitment and higher monthly installments but leads to $0$ monthly payments once the loan is cleared.

2. Long-Term Value vs. Modernity

Do you enjoy having the latest technology and a fresh warranty every few years? Leasing allows you to upgrade frequently without the hassle of selling. However, if you want to build equity and eventually stop making payments altogether, Buying is the superior long-term financial move.

3. Usage and Wear

Most leases come with strict “mileage limits” or “usage hours.” If you exceed these, you will face heavy penalties. If you have a long commute or use equipment intensely, buying gives you the freedom to use the asset as much as you need without watching a clock or odometer.

A Short Example: The 3-Year Car Comparison

Imagine you are looking at a $40,000 luxury sedan.

- Scenario A (Buying): You take a 5-year loan. Your monthly payment is $750. After 3 years, you have paid $27,000 and still owe money, but you have a car that you can eventually own for another decade payment-free.

- Scenario B (Leasing): You sign a 3-year lease. Your monthly payment is $450. After 3 years, you have paid only $16,200. You hand back the keys and walk away. You saved $10,800 in cash flow over those 3 years, but you have no car and must start a new payment cycle for your next vehicle.

The Verdict

Leasing vs. Buying: Which is better for you?

- Choose Buying if: You plan to keep the asset for 5+ years, want to build equity, or don’t want to worry about usage limits.

- Choose Leasing if: You prefer lower monthly payments, want to upgrade to new models every few years, and don’t mind a continuous monthly expense.